Presented at the African Development Bank’s fifth annual Africa Energy Market Place conference, 27 Oct 2021

Hello everybody, we at TBI engaged with government and non-government stakeholders on identifying priorities for Kenya’s energy sector which have gone into our Country Priority Plan, which I will outline now for sustainable energy access.

To better situate us, it’s worth first having a look at the relevant actors in Kenya’s system of electricity provision.

Kenya’s Ministry of Energy is the overarching government body responsible for the energy sector. The Ministry is responsible for developing and implementing policies that create an enabling environment for the efficient operation and growth of Kenya’s energy sector. It has set a target of achieving universal electricity access by 2022.

Regulating the sector is the Energy and Petroleum Regulatory Authority (EPRA).

Kenya Power and Lighting Company (KPLC) is the national power utility which has a monopoly on the distribution of grid electricity in Kenya. KPLC is 50.1% government owned and the remaining ownership is publicly listed on the Nairobi Securities Exchange. It had over 8 million customers as of June 2020.

The Rural Electrification and Renewable Energy Corporation (REREC) was established under the Energy Act of 2019 and has been charged with responsibilities for increasing electricity access in implementing the Rural Electrification Programme, in managing the Rural Electrification Programme Fund, to which ordinary electricity consumers contribute a 5% levy, in developing and updating the rural electrification master plans in consultation with county governments, and in developing and updating the renewable energy master plan. REREC is contracting projects to KPLC, and KPLC is the management agent for the Rural Electrification Scheme (RES) on behalf of the Ministry of Energy.

Since connections under the Rural Electrification Scheme are according to a former auditor general and according to KPLC’s annual report, ‘generally sub-economic since their operational and maintenance costs exceed their revenue,’ the resultant accumulated deficit is recoverable from the Government of Kenya (GOK) as stipulated in the 1973 Mercado agreement signed between KPLC and the Ministry of Energy. There is also power generation at the premises of customers, where the power is sold directly to customers without KPLC as an intermediary. B2C sales occur mainly to rural domestic customers with off grid solar home systems and mini-grids.

So onto the priorities for electrification.

The Kenyan system of electricity provision, including private sector players, have done remarkably well to increase electricity access from 36% in 2014 up to about three quarters of the population today. But that still means that if the Ministry of Energy is to meet its target of universal access to electricity, about a quarter of the population remains to be addressed.

On the other hand, rural connections are a financial challenge for the Kenyan grid power utility, KPLC. According to the most recent KPLC annual report, KPLC’s receivables from last-mile debtors and KPLC liabilities for the last-mile project both increased (2020, Note 28b, p.118).

In addition to that, KPLC had been petitioning the government to release funds owed by the government under the Rural Electrification Scheme. Earlier this year the Auditor General had warned that KPLC risked losing KES 16 billion owed by the government under the scheme since the balance had been long outstanding.

Government supported provision of grid electricity is not of course the only way to achieve universal access to electricity. Where rural customers’ low electricity demand would not amortise lumpy investments into grid transmission and distribution, there are off-grid solutions, and the private sector has proven to be a capable partner in taking the initiative to reach customers with mini-grid and solar home system solutions. However, for investors to participate as much as they usefully can in Kenya’s electrification story, they must have certainty as to where and when the grid is going to expand.

This is where energy demand forecasting at the county government level could come in to assist the Government of Kenya in decide what scale and therefore technology of electricity provision is appropriate for various areas. This is all already embedded into Kenya’s legal frameworks through for example Part II Section 5.5 of the Energy Act 2019 as well as the recommendations of the Presidential Taskforce on the Review of Power Purchase Agreements. Better forecasting at the local level can feed into better planning at the federal level, and better communication to investors in off-grid solutions.

So as far opportunities to achieve sustainable electrification go,

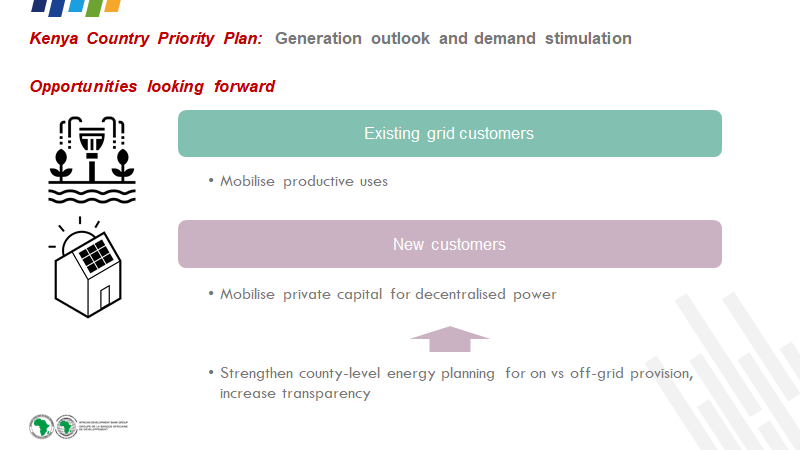

In terms of making KPLC’s existing grid customers less loss-making, there are opportunities to stimulate demand for economically productive uses, such as increasing crop yields with irrigation and improving health outcomes with electrical cooking.

And as sound county government forecasting and judgement feeds into national planning, clarity can be provided to the private sector where the Gov of Kenya does not intend to extend the grid in the medium term in order to mobilise private capital to play a part in Kenya’s electrification story.

With that, I will hand the floor back to Mr Schroth to lead the panel discussion with his co-chair Mr Michael Jordan.

Key take-aways of discussion

- Need for enhanced capacity building and more resource channeling at the county levels for energy demand forecasting

- Ensure county level energy planning is integrated into national planning

- Pricing rationalisation: tariff affordability is a critical issue – need for equalising price paid by mini-grid customers and subsidised lifeline grid connections

- Stable grids required to stimulate investment into appliances and drive growth; appliance financing required

- Mini-grid uncertainty to recover costs when the grid arrives. How will that be implemented in practice?

- Integrated models between grid and off-grid connections to supplement one another, regulation for scale up of mini-grid procurement to reduce costs by 5x through economies of scale