Presented at the African Development Bank’s fifth annual Africa Energy Market Place conference, 28 Oct 2021

Hello, everybody, we at TBI engaged with government and non-government stakeholders on identifying priorities and opportunities for implementation of sector reforms for transmission and distribution in Kenya.

Starting with priorities that we identified, as the diagram at the top left shows, transmission and distribution technical and non-technical losses have been increasing, approaching a quarter of power generated. This obviously puts financial pressure on the power utility KPLC which is not allowed by the regulator to pass through the entirety of the cost of losses to end-consumers, while the Presidential Taskforce on the Review of Power Purchase Agreements has recommended that KPLC seek to reduce the tariff to end consumers by at least a third in the next four months.

Another priority is the completion of ongoing transmission infrastructure projects.

While the diagram on the bottom left hand corner shows that transmission and distribution lines have increased on average across voltage levels by approximately a quarter over the last six years, a number of areas in Kenya are still waiting for better quality electricity. Delays in transmission infrastructure also mean that the cost of delivering power to certain areas such as Laikipia and western Kenya is higher than it should be.

Delays in transmission infrastructure also mean delays in opening power trading opportunities to allow members of the East African Power Pool to become more climate and weather resilient by balancing out variable renewables in the system. This also applies to hydropower which has traditionally been used as a dispatchable source of energy but has become less available due to increasing incidences of drought. Since 94% of Kenya’s grid power is generated from renewable power, it also helps Kenya’s neighbours transition to net zero quicker.

Some ongoing transmission projects include a 400kV AC interconnector between Kenya and Tanzania. On the Kenya side, the project has been delayed by unresolved settlements of compensation for Project Affected People, compounded by COVID19. The Nanyuki-Rumuruti underground 132kV line is currently at the procurement stage. 634km of 500kV DC overhead lines and a converter station constituting the Ethiopia-Kenya Electricity Highway project have substantially been completed and are awaiting final operational acceptance and the start of commercial operations. KETRACO has set aside five transmission line projects to be constructed by Independent Power Producers; among them, two are projects proposed for Africa50. The AfDB also has proposed four further 220kV and 132kV transmission lines under its Transmission System Improvement Project.

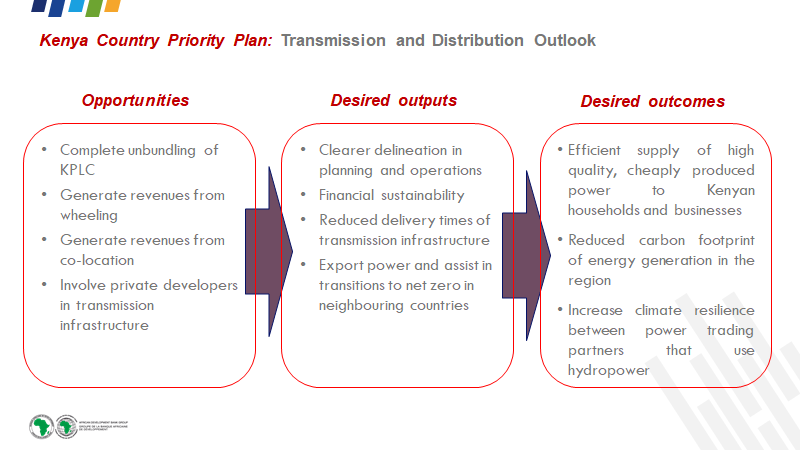

In terms of opportunities going forward in the sector, one area to start is the unbundling of Kenya Power Lighting Company which in addition to being responsible for the maintenance of its distribution network, owns and maintains Kenya’s transmission infrastructure built prior to the creation of KETRACO in 2008. KETRACO is a wholly government owned corporation charged with planning, designing, constructing, owning, operating and maintaining Kenya’s high voltage transmission grid and regional power interconnectors, and is tipped as the favoured institution to become Kenya’s Independent System Operator if the Energy and Petroleum Regulatory Authority decides to push ahead with establishing an ISO.

Unbundling KPLC would allow for a clearer delineation in planning and operations for both KPLC and KETRACO as the potential Independent System Operator.

Other opportunities are to allow transmission infrastructure owners to generate revenues from transporting electric energy from one foreign utility to another, and to generate revenues from leasing excess capacity on fibre optic transmission lines to telecommunications companies, without losing sight of the primary purpose of transmission lines to transport electricity to domestic users, and that revenues are only generated from excess capacity.

Another opportunity is to invite private developers to enter the transmission subsector to, it is hoped, unblock bureaucratic bottlenecks and reduce the delivery times of transmission infrastructure.

The outcomes of these interventions would be higher quality and cheaper energy, reduced embedded carbon resulting from a reduced need for installed capacity within the power trading pool, and increased climate resilience for hydropower dependent power trading partners.

With that, I will hand it over to Mr Batchi Baldeh to commence the panel discussion with Mr Chris Flavin.