Presented at the African Development Bank’s fifth annual Africa Energy Market Place conference, 27 Oct 2021

Hello everybody, we at TBI engaged with government and non-government stakeholders on identifying priorities for Kenya’s energy sector which have gone into our Country Priority Plan, which I will outline now for sustainable power generation.

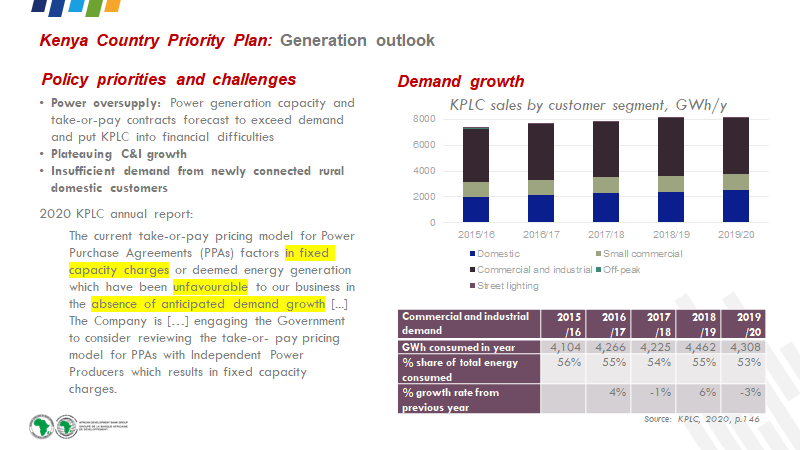

Challenges that we identified for power generation, as the diagram on the right and the table below it show, demand for power generation has been plateauing. This has mainly been due to a slowing of demand growth from commercial and industrial customers who account for more than half of energy demand. Some of this may be explicable by COVID19 restrictions. We’ve also seen a rise in solar captive power that is addressing commercial and industrial customers’ needs for cheap power during sunlight hours, as opposed to the backup diesel generation used when the grid fails. At the same time, the addition of grid connections to rural domestic customers is not going to substantially increase demand for grid electricity.

There are therefore concerns that with the Power Purchase Agreements that the Kenyan partially-state-owned, partially privately owned and listed power utility has signed, there may in the future be an oversupply of power capacity.

This concern was reflected in the power utility’s 2020 annual report, which, in the absence of anticipated demand growth, requested the Government to intervene in reviewing the take-or-pay pricing model for Power Purchase Agreements with Independent Power Producers.

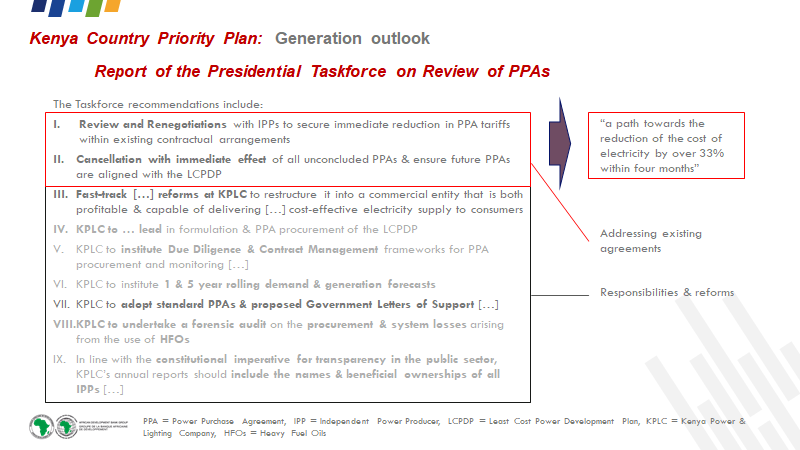

Subsequent to the request, a Presidential Taskforce on the Review of Power Purchase Agreements was convened. Its recommendations were published almost a month ago.

The first two recommendations calling for a review of Power Purchase Agreements and renegotiation of tariffs with Independent Power Producers and calling for the immediate cancellation of all unconcluded Power Purchase Agreements helps set a path towards the Taskforce’s goal of reducing the cost of electricity by over a third in 4 months.

The subsequent recommendations assign responsibilities and call for reforms to address the immediate mismatch between power demand and supply through adjustments to pipeline Power Purchase Agreements and putting in place processes so that the same does not happen in the future.

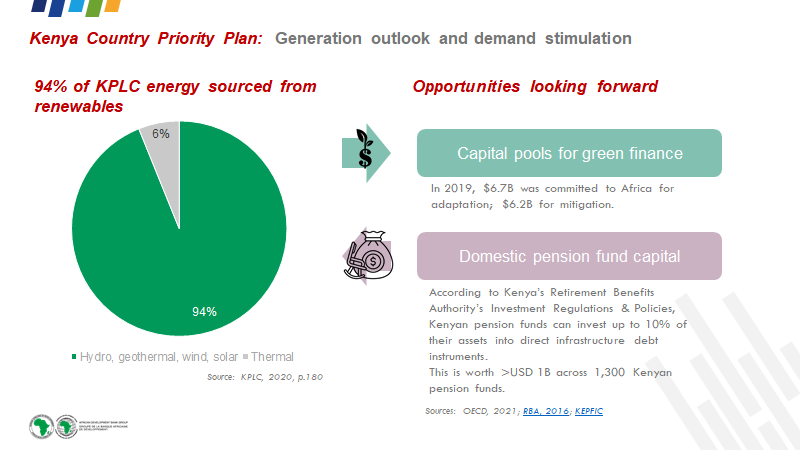

In terms of opportunities looking forward, with 94% of the utility’s energy generated from a diversified array of renewable power sources, there may be opportunities when the utility is seeking to commission new power projects to source cheaper capital from green finance. According to the latest OECD figures, in 2019, $6.2 billion of finance was made available to Africa for climate mitigation. There may also be opportunities to create green capital markets.

Power generation could also possibly be financed by local sources of capital such as domestic pension funds whose long-term investment horizons match the lending requirements of infrastructure investments, and being domestic means that they will not value convertibility risk and certain Kenyan political risks into their cost of capital.

Recent changes to Kenya’s Retirement Benefits Authority’s Investment Regulations and Policies allow Kenyan pension funds to invest up to 10% of their assets into direct infrastructure debt instruments. This means that there is worth more than USD 1 billion of accessible domestic debt capital across 1,300 Kenyan pension funds.

And with that, I would like to hand the session back to Mr Wale Shonibare to lead the discussion with the panelists and his co-chair Mr Vivek Mittal.

Key takeaways of discussion

•Vivek Mittal, AfIDA: Takes 8-10 years to develop power projects in Kenya. The avoidable hold-ups in this process increase costs which are passed through to the utility and end-consumer.

•John Mudany, KenGen: KenGen is committed to renewable energy and foresees growing demand and is keen to spur demand growth via industrial parks located withing Olkaria.

•Rajeev Mahajan, Green Climate Fund: Every country has untapped sources of climate finance in its capital markets. GCF can provide support to unlock this capital for risk mitigation and new markets.

•Bruno de Jesus, Voltalia: Carbon credits can be used to lower the costs to end-consumers. Emphasis on the need to improve the approach on the auction system by making it time bound.

•Anshul Rai, Nigeria Infrastructure Debt Fund: Local currency financing is scalable in a way that foreign investment is not. It significantly reduces the need for government support mechanisms and the impact on currency depreciation and inflation which cannot be ignored for long term infrastructure projects.

•Ngatia Kirungie, Kenya Pension Funds Investment Consortium: The first step in mobilizing Kenyan pension fund finance has been taken with respect to allowing for 10% direct investment in infrastructure debt instruments. The next steps will involve a) getting clarity on what renegotiation of tariffs mean for investors in the sector and b) educating pension fund trustees about the risks of investing directly into infrastructure.